From Startup Stock to $15 Million Tax-Free: QSBS Explained for 2026

Aaron White, CFP®

Head of Investor Solutions

Christopher Karachale

Partner at Hanson Bridgett LLP

Origins of Section 1202

In 1993, Congress introduced Qualified Small Business Stock (QSBS) under Section 1202 of the Internal Revenue Code to encourage long-term investment in emerging companies. The policy aim was simple: reward those who fund innovation by allowing them to exclude a substantial portion of their capital gains when they eventually sell the stock.

Initially, the benefit was modest: only 50% of the gain was excluded, and alternative minimum tax (AMT) adjustments often clawed back much of the advantage. Over the years, successive reforms raised the exclusion to 75%, and then, for stock acquired after September 27, 2010, the exclusion reached 100%, permanently exempting those gains from both federal capital gains and AMT.

This framework, though narrow, became one of the most beneficial incentives in the tax code for founders, early employees, and investors in high-growth C-corporations.

What Qualifies as QSBS

To benefit under Section 1202, both the company and the stockholder must meet a strict checklist:

- Entity type: The company must be a domestic C-corporation, without a previous S-election.

- Gross assets: The company must have aggregate gross assets below a specific threshold, at stock issuance and immediately afterwards:

- <$50 million: for stock issued on or before July 4, 2025

- <$75 million: for stock issued after July 4, 2025

-

- Aggregate gross assets = cash plus the adjusted tax basis of other property held by the corporation. The valuation of the company is not typically relevant when determining QSBS status at issuance.

- Active business: At least 80% of the corporation’s assets must be used in a qualified trade or business. Professional service companies and several other industries are disqualified (e.g. law, accounting, consulting, banking, insurance, and farming).

- Original issuance: The investor must acquire shares directly from the company in exchange for cash, property (other than stock), or as compensation for services.

- Holding period: Shares must be held more than five years for stock issued before July 5, 2025. Partial exclusions are available for stock issued after July 4, 2025, 50% for shares held 3+ years and 75% for shares held 4+ years.

Benefits

For qualifying shareholders, the math is striking:

- 0% federal capital-gains tax on the greater of:

- $10 million or 10× basis: for stock issued on or before July 4, 2025

- $15 million or 10× basis: for stock issued after July 4, 2025

- No AMT or Net Investment Income Tax (NIIT) on excluded gains, subject to the limitations discussed later in the article.

- 0% state level taxes in 40+ states: Many states conform to Federal tax law for QSBS benefits or have no state income tax.

- California, New Jersey, Pennsylvania and several other states do not conform to federal law for QSBS benefits and would likely therefore be subject to taxation at the state level.

In aggregate, the QSBS exclusion can reduce the effective federal tax rate on a successful exit from 23.8% to 0%—potentially saving millions for founders and early investors.

Practical Planning Considerations

QSBS benefits depend on careful planning and documentation, and the following considerations can materially affect eligibility and outcomes.

- Confirm entity qualification: Ensure the company is a C-corp and has maintained gross assets under the applicable threshold. LLC to C-corp conversions may qualify as QSBS, however a prior S-election is a disqualifying event.

- Track acquisition date and basis: Keep detailed records of when and how stock was acquired, especially when options, RSUs, or ESPP purchases are involved.

- Mind the holding period: Stock acquired through an option exercise or RSU settlement starts the five-year clock on that date, not on the grant date.

-

💡 Important callout: For Incentive Stock Options (ISO) the five-year clock starts from the date of vest, not the date of exercise. An important distinction for early exercise planning with 83(b) elections.

-

- Disqualifications: Contributions of QSBS to a partnership (e.g. exchange fund) will result in a loss of QSBS status. Corporate recapitalizations, redemptions, or secondary transfers can also jeopardize QSBS status.

- State alignment: State-level treatment can meaningfully affect after-tax proceeds. See below for a full breakdown.

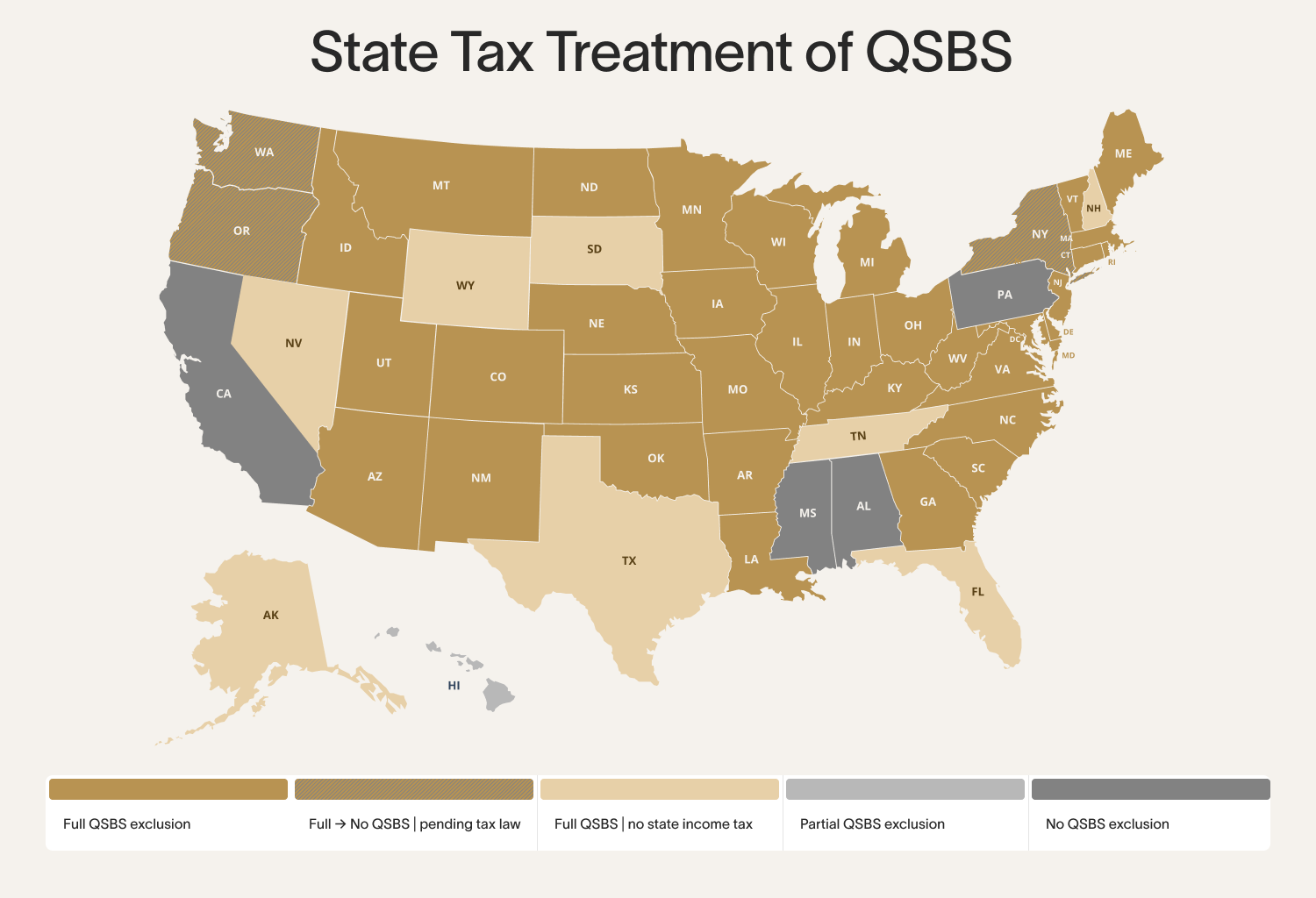

State Taxes

States vary widely in how they conform to federal QSBS rules, making state tax treatment a critical planning factor.

- No QSBS: California, Pennsylvania, Mississippi, and Alabama

- New Jersey: pre-2026 stock sales only

- Washington DC: decoupled from federal law on November 6, 2025

- Partial QSBS: Hawaii (50% exclusion)

- Full QSBS: New Jersey (2026 onward) and all other states align with federal tax law

- Pending Tax Law Changes: Washington, Oregon, and New York are considering new legislation that would eliminate state level QSBS benefits.

2025 Expansion

The One Big Beautiful Bill Act (July 2025) modernized QSBS for today’s venture economy.

Key changes include:

- Increasing the gross-asset threshold to $75 million, expanding eligibility for later-stage growth companies.

- Clarified treatment of convertible instruments, allowing SAFE notes and post-conversion preferred stock to count as “original issuance.”

- Simplified documentation: corporations can now issue a QSBS eligibility statement to investors, easing future diligence.

Together, these updates broaden the reach of Section 1202 while addressing years of uncertainty that limited its use among institutional investors and startups alike.

Source: https://irs.gov/newsroom/one-big-beautiful-bill-provisions

Putting It All Together

The renewed QSBS regime represents a rare bipartisan win for entrepreneurship: rewarding innovation, deepening early-stage capital, and encouraging patient holding periods.For advisors and founders alike, the implications are profound:

- Startups can now scale further before losing eligibility.

- Employees can exercise earlier and hold longer with clearer guidance.

- Investors can reinvest gains without tripping the clock.

As with exchange funds, QSBS planning thrives on precision. The benefit is binary: you either qualify or you don’t. The difference can mean millions. For founders, early employees, and angel investors, this is the time to revisit your cap table and confirm your eligibility before your next round or liquidity event.

Thanks to Christopher Karachale for his insights on the article — if you have questions on QSBS planning, he's a great resource. Christopher can be reached at: CKarachale@hansonbridgett.com

This article is for general informational and educational purposes only and does not constitute tax, legal, or investment advice. If you have questions please work with a qualified tax or legal professional. Nothing in this article should be construed as a recommendation, solicitation, or offer to buy or sell any security or to engage in any specific tax-planning strategy.

The application of Section 1202 and related provisions depends heavily on individual facts and circumstances, including but not limited to the issuer's corporate history, asset composition, business activities, the timing and manner of stock acquisition, holding period, state of residence, and the taxpayer's broader tax position. Statements about specific tax outcomes (e.g., "0% federal capital-gains tax," "$10M/$15M exclusion") describe the statutory framework — they are not predictions of any individual taxpayer's outcome.

Federal and state tax law in this area is changing rapidly. Information in this article reflects sources believed to be reliable as of May 2026, including the One Big Beautiful Bill Act but is not updated automatically and is not guaranteed to be current, complete, or accurate at the time you read it. State-level conformity in particular is being actively revisited in multiple jurisdictions.

Cache and Hanson Bridgett LLP are unaffiliated companies.

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.