Generate tax losses to transition your appreciated portfolio

diversify your winning stocks and manage taxes,

now and down the road.

Designed to generate offsets across more market conditions than direct indexing.

You own the stock, and every long/short position, directly in your brokerage.

Starting at 0.50% advisory fee and 0.17% financing costs (post-tax).

"One of the most important parts of my decision was trust.

With Cache, I felt I was working with a company that has high integrity and would take good care of my investments."

When to consider a

tax-aware long/short strategy

Reduce concentration gradually while generating tax offsets, without selling all at once.

Had a big year from stocks, RSUs, or active trading? Harvest losses to offset those gains, with any excess carried forward.

Build potential tax offsets ahead of an IPO or planned diversification, in coordination with your tax advisor.

Use it as a “long-short direct indexing” solution. Manage gains over time, while staying invested in the market.

Cache and BKLN partnered to build a long/short solution that’s more accessible and easy-to-use.

BKLN is a subsidiary of Nuveen, one of the largest financial institutions in the U.S. with over $1.4 trillion in AUM.

See how you could benefit

How the strategy works

A step-by-step overview of how the Cache Long/Short tax-loss harvesting strategy is structured and managed over time.

How Tax-Aware Long/Short works

Still have questions about Cache Long/Short?

Watch Aaron explain how it works

Why investors choose Cache Long/Short

A professional-grade tax-loss harvesting engine for your personal portfolio.

You own the underlying securities directly, in your own brokerage account, not a pooled fund.

Trading, factor rebalancing, and tax-aware execution are handled by BKLN’s experienced portfolio management team.

Open and fund your account entirely online, on your own timeline. See your portfolio and activity with a real-time digital experience.

Built on a sophisticated tax-aware engine that seeks to avoid wash sales against stocks you hold in your portfolio.

Core extensions offered

Extensions use margin borrowing and short sales, which increase risk, especially during volatile markets

Returns may deviate from benchmark performance, especially at higher borrowing levels.

Loss harvesting is not guaranteed, and varies by market conditions.

Self-serve onboarding and a fully digital experience

Cache Long/Short is designed to help modern investors manage their tax-aware investments with ease.

Choose your goal, select your benchmark and set your extension size (borrowing %). You’ll also go through a risk assessment to ensure you are a fit.

Open your managed Schwab account (held in your name, joint, or trust) and fund the account with your core assets.

Let the long/short engine work for you. The portfolio runs continuously, losses are harvested systematically, as volatility may create opportunities to realize tax offsets over time.

An active strategy,

managed by an expert team

Guided by decades of experience navigating changing market conditions.

CEO & Chief Investment Officer

MD at Goldman Sachs, New York Fed Economist. NYU Adjunct Professor. Harvard, MIT.

CHIEF EQUITY STRATEGIST

Former Portfolio Manager at BlackRock. Professor at Yale and NYU. MIT.

Chief Quant & Co-CTO

Quantitative Researcher at hedge funds and Credit Suisse. UChicago.

Head of Trading

Quantitative trading at Citadel and Goldman Sachs. Carnegie Mellon.

Why investors, advisors, and executives turn to Cache to diversify

"Cache solved a problem I'd been facing for years - how to diversify after over a decade of accumulating my previous company's stock without a massive tax hit. Since my first investment, I've continued to contribute additional funds, and I sleep better now knowing I'm finally diversified using a platform I trust."

"Cache brought simplicity and transparency to the exchange fund process that was traditionally complex and opaque. It made diversifying my concentrated portfolio simple."

"Cache has built THE PERFECT PRODUCT for tech professionals with concentrated stock positions — and their client service is second to none."

"Cache enables investors like our clients to eliminate single stock risk without paying a hefty diversification tax."

"The transparency in pricing and simplicity in design makes sophisticated investing straightforward and user-friendly."

"I feel great about participating in the exchange fund because I'm more in control and I'm more diversified.

"Cache made the entire investment process incredibly simple and straightforward. Not only is their product truly amazing, but the exceptional customer service makes them the absolute best in the industry. Their innovative approach sets them far ahead of competitors."

"I tried to do an exchange fund before Cache, and it was like trying to join a cult. Little info, little transparency, and little confidence with cost and charges. Cache changed all that!"

"Cache has put together an experienced, professional team that brings the tax efficient strategies of the ultra-wealthy to the masses."

"Ever since I learned about exchange funds I've been looking for something like Cache - a simple, transparent and accessible product to diversify tax efficiently."

"Cache provides a great service that just works. Their low-friction delivery of complex financial products made becoming a client an obvious choice."

Cache does not pay for testimonials or endorsements

Testimonials are provided by individuals identified as Clients above. Endorsements are provided by Advisors identified above. Advisors are not direct clients of Cache Advisors, LLC unless otherwise specified, but collaborate with Cache Advisors, LLC on behalf of their firm's clients. The testimonials and endorsements may not accurately represent the experiences of others, and there is no guarantee of future performance or success. A conflict of interest exists as the Advisors have a current business relationship with Cache. Neither Clients nor Advisors were compensated for these statements.

FAQs

About Long/Shorts

(X)

What is Cache Long/Short?

Who is this strategy for (and not for)?

When does Cache Long/Short make sense?

What’s the main benefit of Cache Long/Short?

Is this a hedge fund?

How does Cache Long/Short fit alongside Exchange Funds?

How It Works

(X)

How does Cache Long/Short work, in simple terms?

How is this different from traditional tax-loss harvesting or direct indexing?

What kinds of gains can harvested losses offset?

Taxes & Outcomes

(X)

Are results guaranteed?

How long does it typically take to see tax benefits?

What happens if tax laws change?

Risk & Structure

(X)

Do I need margin approval?

What risks should I understand?

Can I lose more than I invest?

Liquidity, Access & Transitions

(X)

How liquid is the strategy?

How do I transition or exit?

Compliance & Operational Safeguards

(X)

How can Cache help me stay compliant with employer trading rules?

How does the program help prevent wash sales across accounts?

Can I exclude certain stocks or restricted lists?

Trust, Custody & Logistics

(X)

Within Cache Long/Short, who does what?

What happens if Cache or Brooklyn can't continue operations?

What reporting and tax forms do I receive?

Costs & Tradeoffs

(X)

What does this strategy cost?

How should I think about costs vs. potential tax savings?

What are the tradeoffs compared to doing nothing or selling outright?

QUESTION

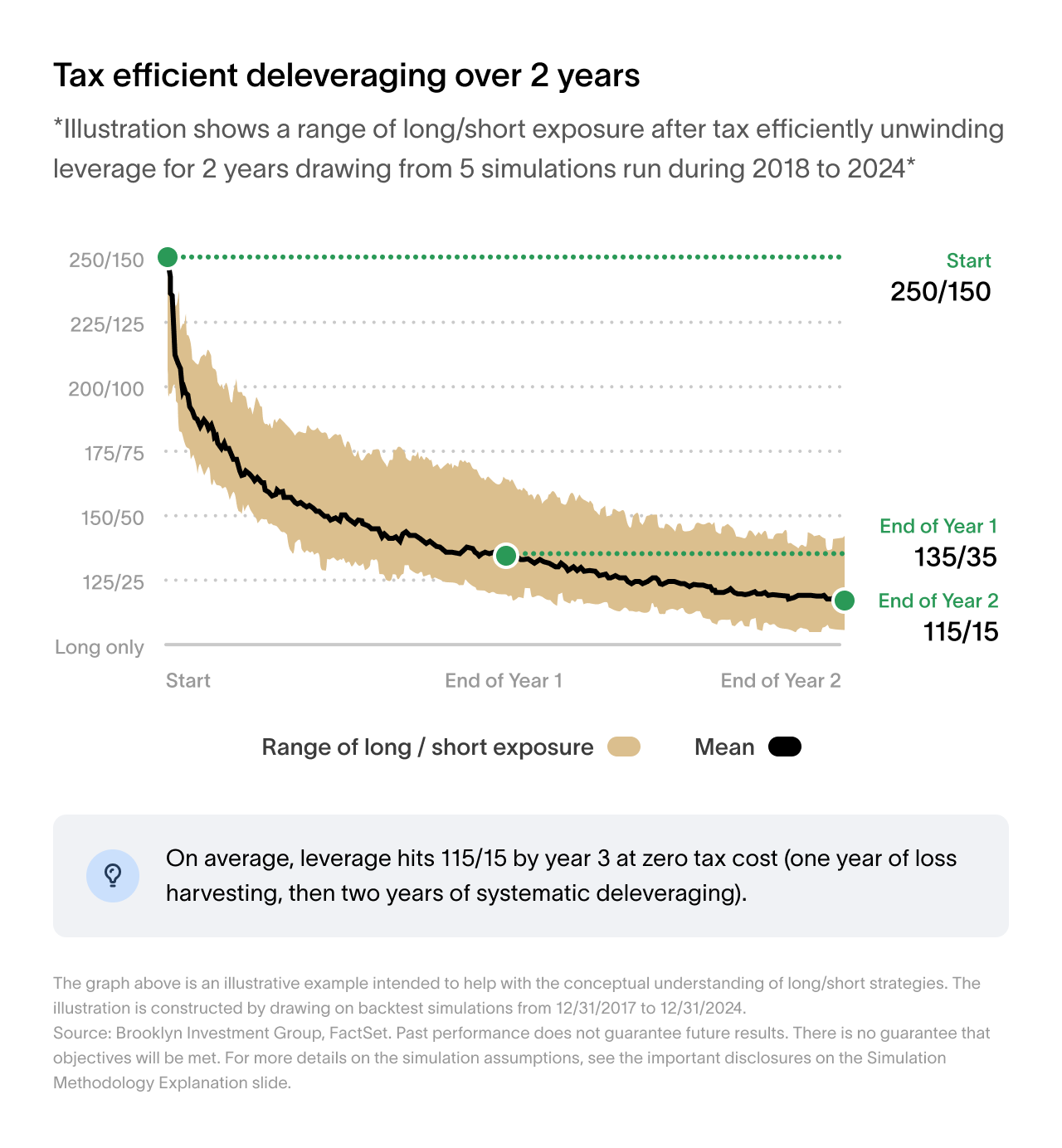

How do I transition or exit from Cache Long/Short?

Exiting is deliberate and tax-aware, not instantaneous. Transitions ideally occur gradually, which helps avoid triggering a large immediate tax bill and allows previously harvested losses to offset gains as they’re realized.

You decide when to begin. BKLN manages execution by gradually reducing the long/short extension and moving the portfolio toward an unlevered, diversified core. Some investors unwind slowly to spread taxes across multiple years. Others accelerate if outside liquidity (from an IPO, business sale, or other event) gives them flexibility to absorb gains faster.

There’s no fixed timeline, but most investors should expect several years, not months. Exiting too quickly compresses the tax benefit. To preserve efficiency, exits should be managed within the strategy. Unwinding positions independently can result in unintended gain realization.

Tax outcomes vary by individual circumstances and market conditions. Consult your tax advisor when planning an exit.

Ready to see if Cache Long/Short is right for you?

A complete

diversification toolkit

Access all the tools you need to diversify your concentrated stocks in one place.

Cost basis of your shares

For shares with significant gains and typically a low cost basis

For managing transitions from shares with moderate gains

For diversifying shares with low embedded gains