Cache Long/Short: A Client Case Study, Two Months In

Srikanth Narayan

Founder and CEO

Why did we build Cache Long/Short? Because we don't think concentrated stock is a one-product problem. Cache Long/Short can provide investors with more flexibility, while reducing concentration risk and harvesting losses to offset gains along the way.

If you’re new to the concept of long/short strategies, check out our Complete Guide to Tax-Aware Long/Short Investing.

The Setup

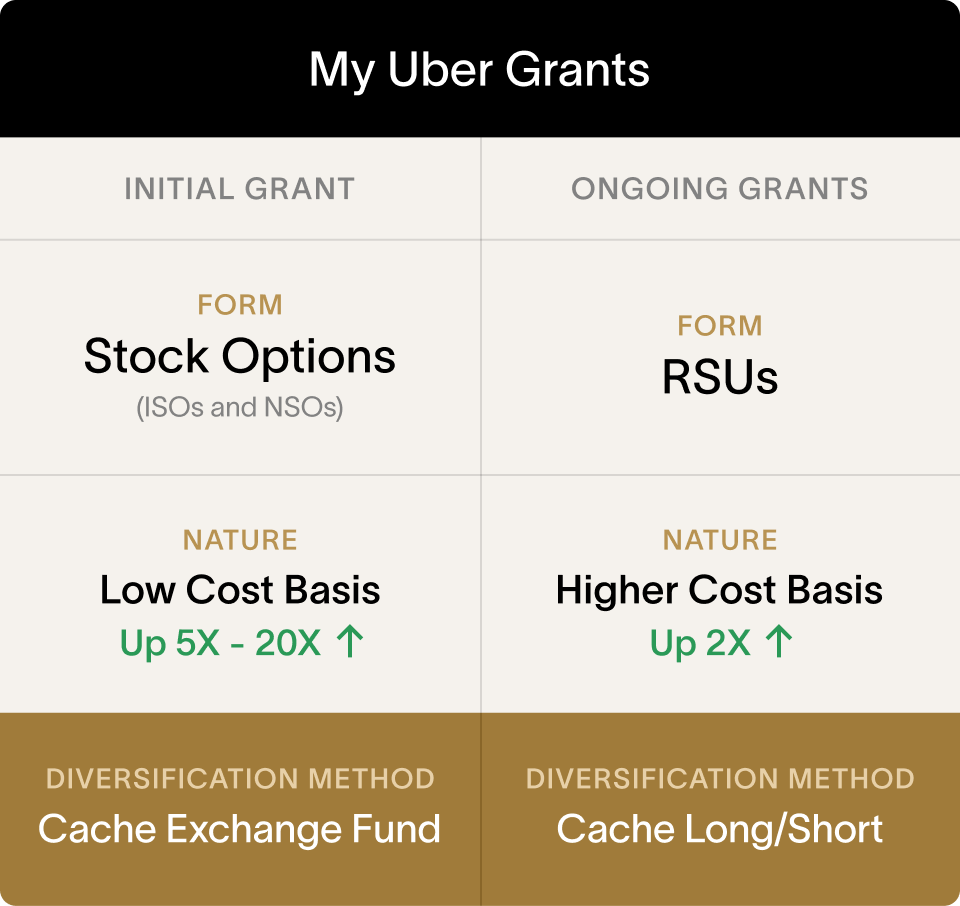

In late March, I funded my account with roughly $1M of assets: a portion of my concentrated UBER position, a highly appreciated GLD position, and several ETFs and cash as collateral.

I worked at Uber from 2014 to 2020. My earliest Uber grants from stock options were highly appreciated, and I used the Cache Exchange Fund to diversify some of these holdings. Ongoing grants, issued as RSUs, had a higher cost basis, making them well-suited for Cache Long/Short.

That distinction matters. We often hear investors talk about concentrated stock as though it were a single position. In practice, different lots can have very different tax characteristics. The right strategy for deeply appreciated options may not be the right strategy for ones with higher basis.

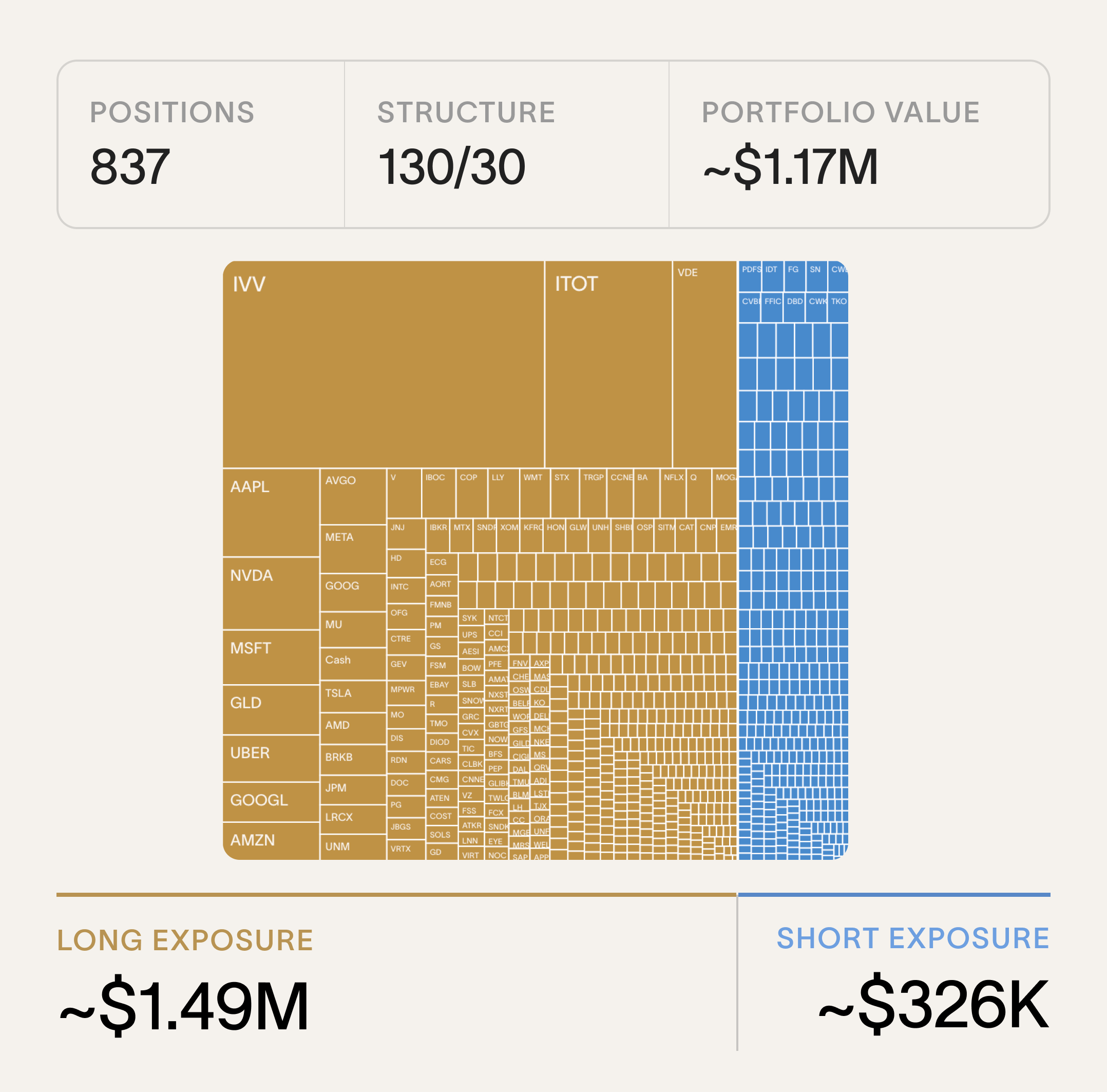

My Cache Long/Short Portfolio

About two months in, the portfolio held roughly $1.2M across 837 positions, running a 130/30 long/short strategy benchmarked to the S&P 500.

Tax-efficient Diversification

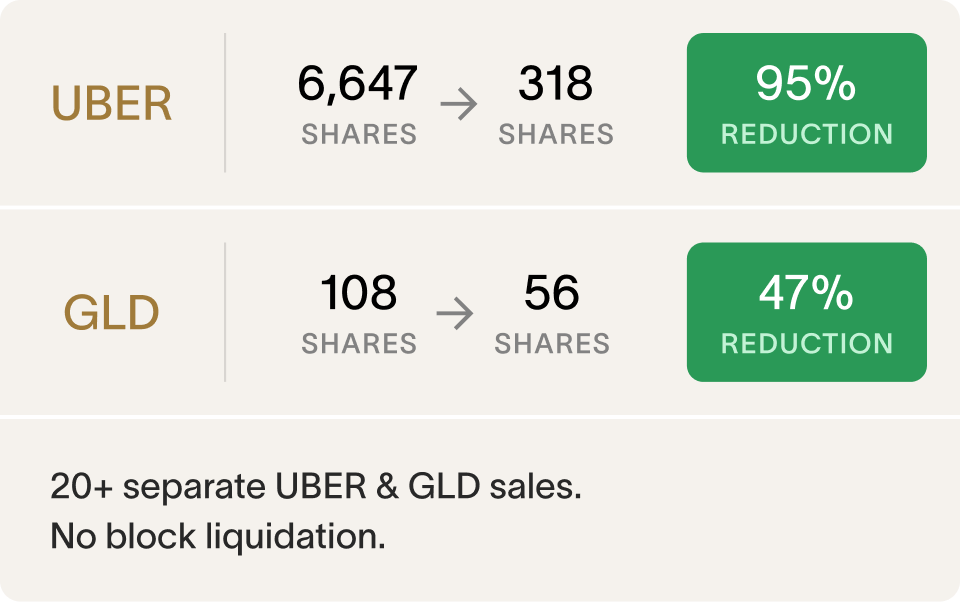

The Uber position is largely gone: down from 6,647 shares ($465K) to 318 shares ($22.6K), a 95% reduction across 20 separate trades. Those trades realized about $200K in gains. The purpose of the strategy was to generate losses elsewhere in the portfolio that could offset those gains.

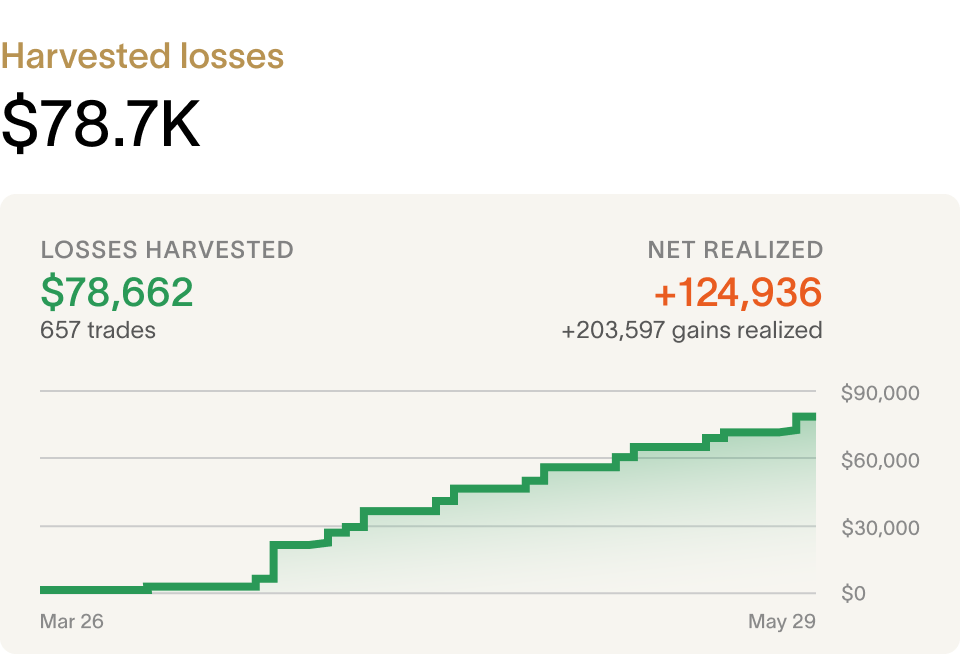

Across 854 transactions, the strategy harvested $78.7K in losses. Nearly all of the gains realized from selling UBER and GLD were long-term, while nearly all harvested losses were short-term. That's generally the most valuable tax outcome.

The Benefits

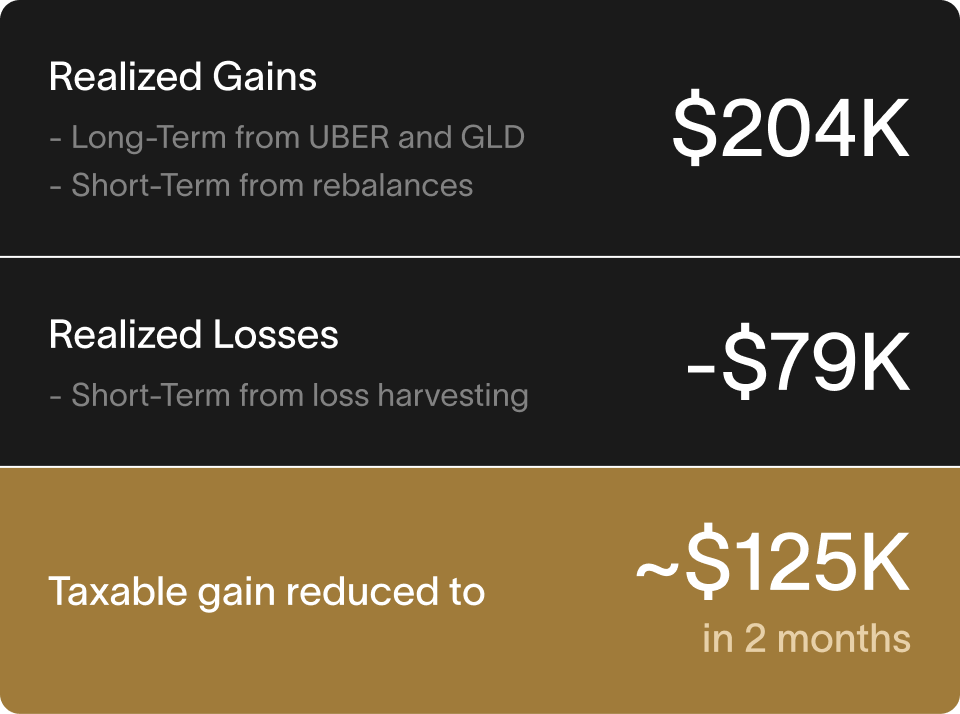

Taxable long-term gains fall from roughly $195K to $125K in just two months, and as of this writing the strategy still had several months left in the year to continue harvesting.

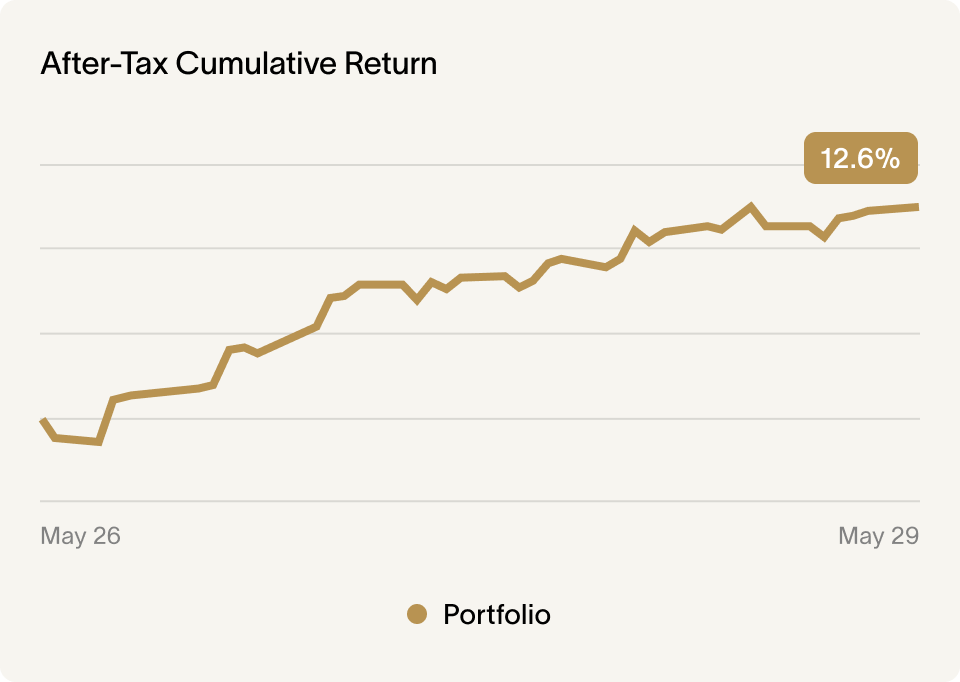

Given my legacy holdings, performance is compared against an adjusted benchmark that factors in these weights. Since we started, the strategy is up 12.6%, slightly ahead of the adjusted benchmark on an after-tax basis. The tax-loss harvesting didn't require stepping out of the market.

Over the first two months, the strategy generated roughly $40K of losses per month. Future loss generation will depend on market conditions, and a substantial portion of the remaining taxable gain from the UBER unwind ideally may be offset before year-end.

One common misconception is that tax-loss harvesting eliminates taxes altogether.

It does not.

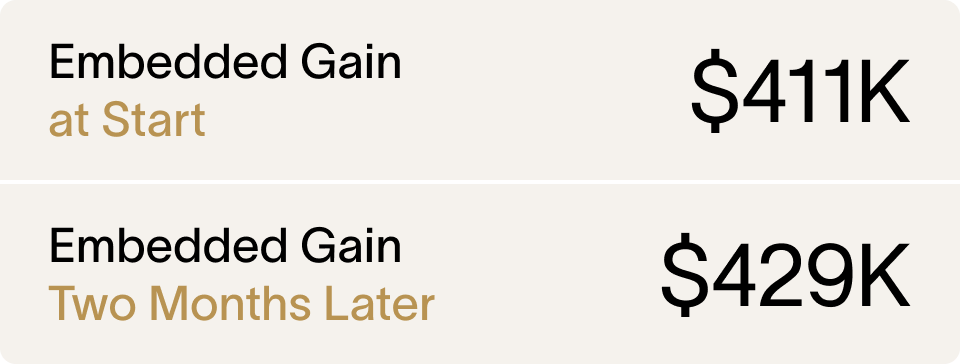

The gain is simply deferred rather than eliminated. My portfolio began with roughly $411K of embedded gains. After realizing gains, harvesting losses, and remaining invested, the portfolio still contains roughly $429K of embedded gains. The value comes from when and how those gains are recognized.

Over two months, roughly $500K of concentrated UBER and GLD exposure moved into a broadly diversified portfolio, while the strategy harvested meaningful losses along the way.

Running the strategy in my own account reinforced something we've long believed: concentrated stock is rarely a single problem with a single solution. In my planning, my earliest Uber grants were better candidates for an Exchange Fund. Later RSU grants proved well-suited for Long/Short.

Different lots call for different tools.

If you're weighing how to manage a concentrated position, you can model your own situation with our Long/Short calculator, learn more on the Long/Short product page, or talk to our team.

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.